Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Helios Technologies, Inc. (NASDAQ:HLIO) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

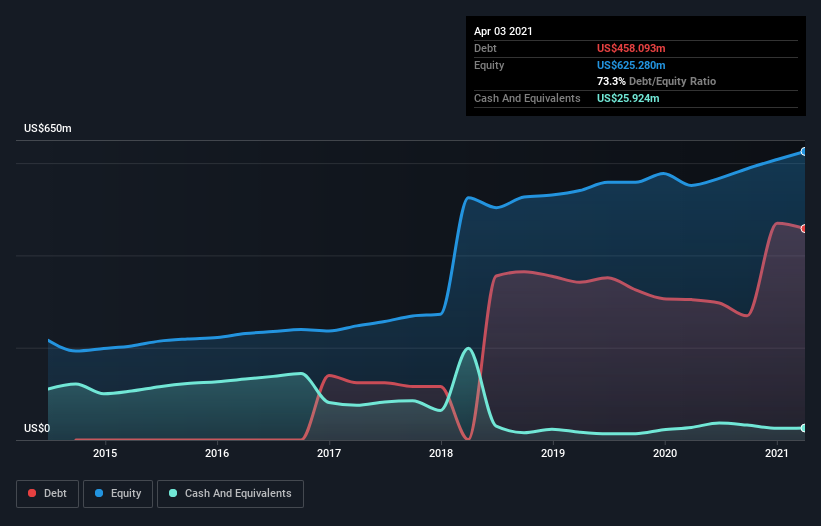

What Is Helios Technologies’s Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of April 2021 Helios Technologies had US$458.1m of debt, an increase on US$304.3m, over one year. However, it does have US$25.9m in cash offsetting this, leading to net debt of about US$432.2m.

A Look At Helios Technologies’ Liabilities

We can see from the most recent balance sheet that Helios Technologies had liabilities of US$142.1m falling due within a year, and liabilities of US$544.1m due beyond that. On the other hand, it had cash of US$25.9m and US$127.2m worth of receivables due within a year. So its liabilities total US$533.1m more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Helios Technologies is worth US$2.32b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Helios Technologies’s debt is 3.1 times its EBITDA, and its EBIT cover its interest expense 6.1 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Importantly Helios Technologies’s EBIT was essentially flat over the last twelve months. Ideally it can diminish its debt load by kick-starting earnings growth. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Helios Technologies’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Helios Technologies produced sturdy free cash flow equating to 76% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Happily, Helios Technologies’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. But truth be told we feel its net debt to EBITDA does undermine this impression a bit. All these things considered, it appears that Helios Technologies can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.