Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Global Ship Lease, Inc. (NYSE:GSL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Global Ship Lease Carry?

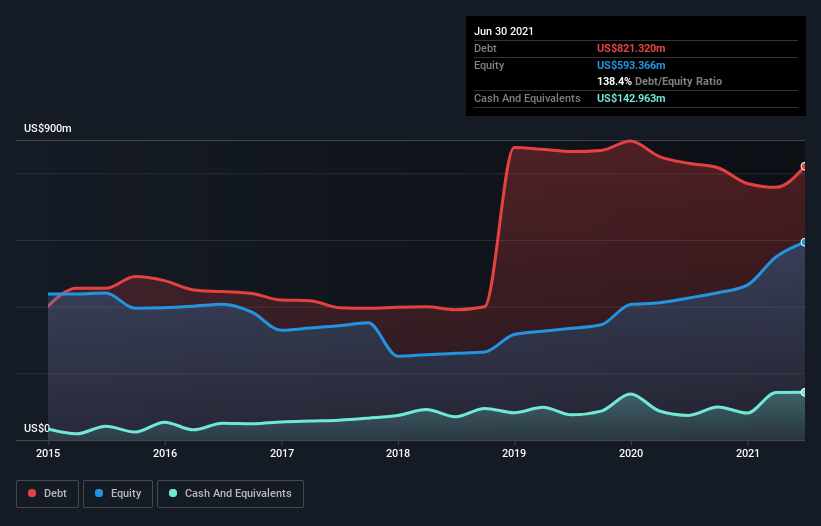

As you can see below, Global Ship Lease had US$821.3m of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$143.0m in cash, and so its net debt is US$678.4m.

How Healthy Is Global Ship Lease’s Balance Sheet?

The latest balance sheet data shows that Global Ship Lease had liabilities of US$128.8m due within a year, and liabilities of US$730.6m falling due after that. Offsetting this, it had US$143.0m in cash and US$4.88m in receivables that were due within 12 months. So it has liabilities totalling US$711.5m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$800.0m, so it does suggest shareholders should keep an eye on Global Ship Lease’s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn’t worry about Global Ship Lease’s net debt to EBITDA ratio of 4.2, we think its super-low interest cover of 2.0 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Fortunately, Global Ship Lease grew its EBIT by 7.2% in the last year, slowly shrinking its debt relative to earnings. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Global Ship Lease’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Global Ship Lease reported free cash flow worth 10% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Mulling over Global Ship Lease’s attempt at covering its interest expense with its EBIT, we’re certainly not enthusiastic. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Global Ship Lease’s use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There’s no doubt that we learn most about debt from the balance sheet.