The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Gevo, Inc. (NASDAQ:GEVO) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Gevo Carry?

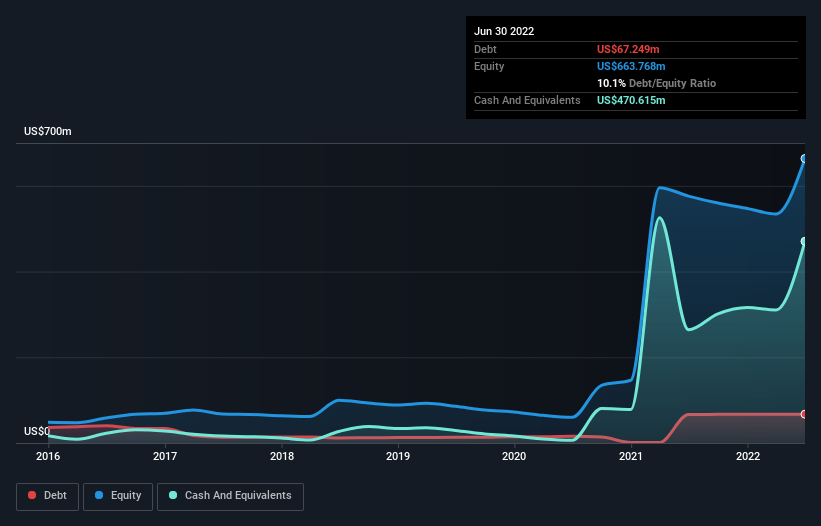

The chart below, which you can click on for greater detail, shows that Gevo had US$67.2m in debt in June 2022; about the same as the year before. But on the other hand it also has US$470.6m in cash, leading to a US$403.4m net cash position.

A Look At Gevo’s Liabilities

The latest balance sheet data shows that Gevo had liabilities of US$25.6m due within a year, and liabilities of US$85.2m falling due after that. Offsetting these obligations, it had cash of US$470.6m as well as receivables valued at US$1.61m due within 12 months. So it actually has US$361.4m more liquid assets than total liabilities.

This luscious liquidity implies that Gevo’s balance sheet is sturdy like a giant sequoia tree. Having regard to this fact, we think its balance sheet is as strong as an ox. Simply put, the fact that Gevo has more cash than debt is arguably a good indication that it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Gevo’s ability to maintain a healthy balance sheet going forward.

Given its lack of meaningful operating revenue, Gevo shareholders no doubt hope it can fund itself until it can sell some combustibles.

So How Risky Is Gevo?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Gevo had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$142m and booked a US$60m accounting loss. With only US$403.4m on the balance sheet, it would appear that its going to need to raise capital again soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn’t produce free cash flow regularly.