David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Fortress Biotech, Inc. (NASDAQ:FBIO) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Fortress Biotech’s Net Debt?

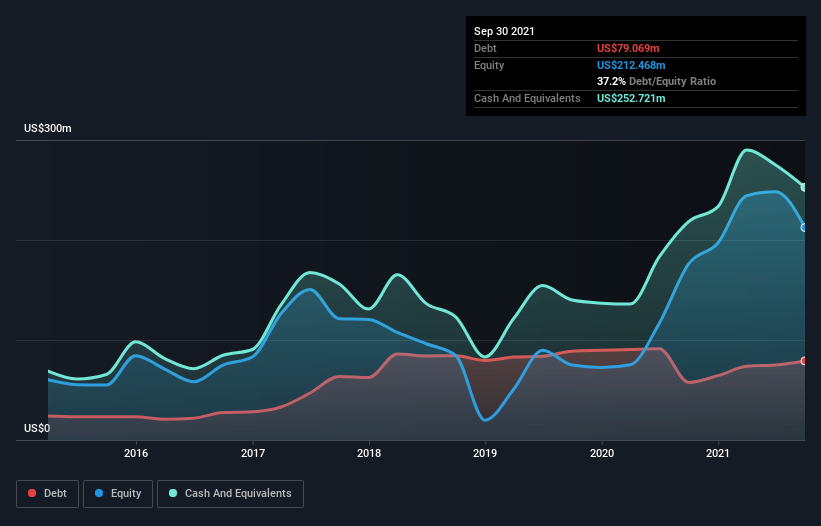

The image below, which you can click on for greater detail, shows that at September 2021 Fortress Biotech had debt of US$79.1m, up from US$57.6m in one year. But on the other hand it also has US$252.7m in cash, leading to a US$173.7m net cash position.

A Look At Fortress Biotech’s Liabilities

Zooming in on the latest balance sheet data, we can see that Fortress Biotech had liabilities of US$103.2m due within 12 months and liabilities of US$92.2m due beyond that. Offsetting these obligations, it had cash of US$252.7m as well as receivables valued at US$32.7m due within 12 months. So it actually has US$90.0m more liquid assets than total liabilities.

This surplus liquidity suggests that Fortress Biotech’s balance sheet could take a hit just as well as Homer Simpson’s head can take a punch. Having regard to this fact, we think its balance sheet is as strong as an ox. Succinctly put, Fortress Biotech boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Fortress Biotech’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Fortress Biotech reported revenue of US$64m, which is a gain of 50%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Fortress Biotech?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Fortress Biotech lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$113m of cash and made a loss of US$38m. But at least it has US$173.7m on the balance sheet to spend on growth, near-term. Fortress Biotech’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start.