Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Ferrari N.V. (NYSE:RACE) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

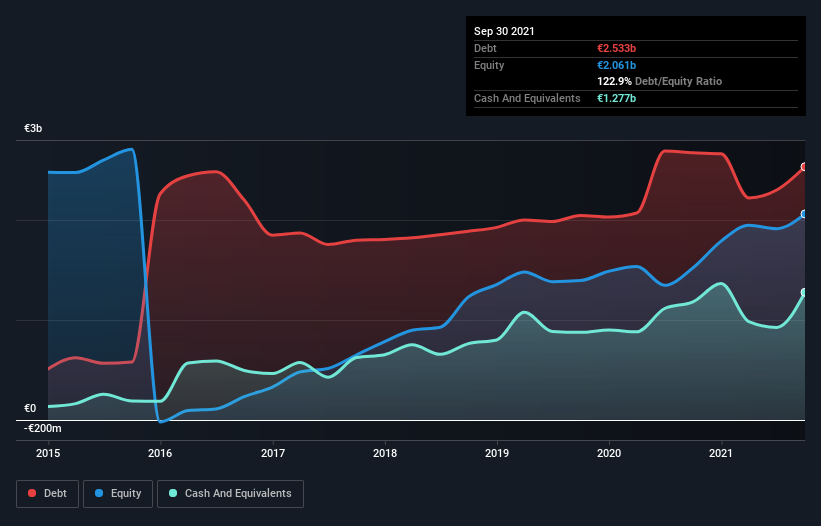

What Is Ferrari’s Net Debt?

As you can see below, Ferrari had €2.53b of debt at September 2021, down from €2.67b a year prior. However, it also had €1.28b in cash, and so its net debt is €1.26b.

How Strong Is Ferrari’s Balance Sheet?

The latest balance sheet data shows that Ferrari had liabilities of €1.26b due within a year, and liabilities of €3.29b falling due after that. Offsetting these obligations, it had cash of €1.28b as well as receivables valued at €233.6m due within 12 months. So its liabilities total €3.04b more than the combination of its cash and short-term receivables.

Given Ferrari has a humongous market capitalization of €42.3b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Ferrari’s net debt is only 0.98 times its EBITDA. And its EBIT covers its interest expense a whopping 25.9 times over. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Ferrari has boosted its EBIT by 52%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ferrari can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Ferrari recorded free cash flow of 47% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Happily, Ferrari’s impressive interest cover implies it has the upper hand on its debt. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Looking at the bigger picture, we think Ferrari’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start.