David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Eagle Pharmaceuticals, Inc. (NASDAQ:EGRX) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Eagle Pharmaceuticals’s Net Debt?

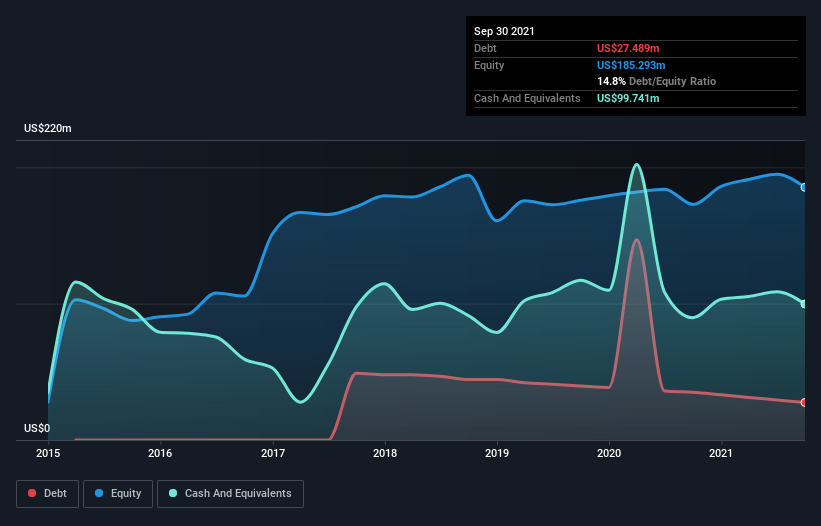

As you can see below, Eagle Pharmaceuticals had US$27.5m of debt at September 2021, down from US$35.0m a year prior. But it also has US$99.7m in cash to offset that, meaning it has US$72.3m net cash.

How Healthy Is Eagle Pharmaceuticals’ Balance Sheet?

The latest balance sheet data shows that Eagle Pharmaceuticals had liabilities of US$48.4m due within a year, and liabilities of US$22.5m falling due after that. Offsetting this, it had US$99.7m in cash and US$51.6m in receivables that were due within 12 months. So it actually has US$80.4m more liquid assets than total liabilities.

This surplus suggests that Eagle Pharmaceuticals has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Eagle Pharmaceuticals has more cash than debt is arguably a good indication that it can manage its debt safely.

Importantly, Eagle Pharmaceuticals’s EBIT fell a jaw-dropping 85% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Eagle Pharmaceuticals can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. Eagle Pharmaceuticals may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Eagle Pharmaceuticals actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While it is always sensible to investigate a company’s debt, in this case Eagle Pharmaceuticals has US$72.3m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 239% of that EBIT to free cash flow, bringing in US$39m. So we are not troubled with Eagle Pharmaceuticals’s debt use. The balance sheet is clearly the area to focus on when you are analysing debt.