Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Clean Energy Fuels Corp. (NASDAQ:CLNE) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Clean Energy Fuels’s Debt?

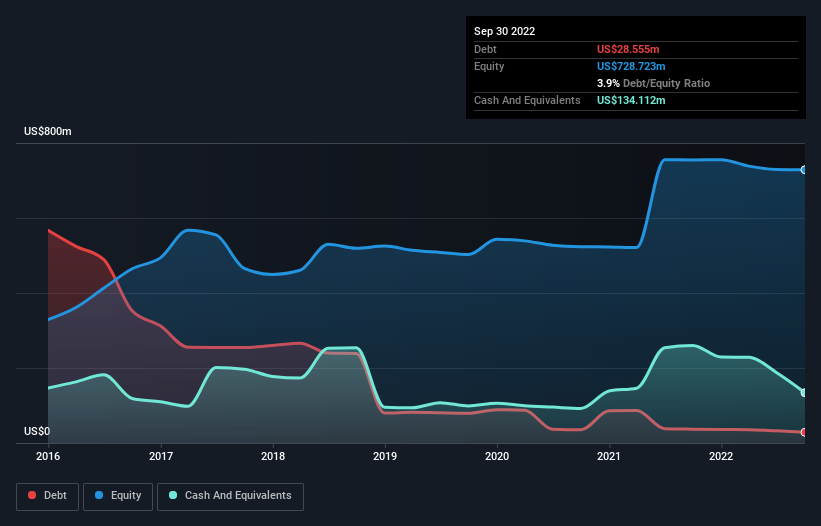

The image below, which you can click on for greater detail, shows that Clean Energy Fuels had debt of US$28.6m at the end of September 2022, a reduction from US$37.0m over a year. However, it does have US$134.1m in cash offsetting this, leading to net cash of US$105.6m.

How Strong Is Clean Energy Fuels’ Balance Sheet?

According to the last reported balance sheet, Clean Energy Fuels had liabilities of US$134.1m due within 12 months, and liabilities of US$78.6m due beyond 12 months. Offsetting this, it had US$134.1m in cash and US$129.3m in receivables that were due within 12 months. So it can boast US$50.7m more liquid assets than total liabilities.

This short term liquidity is a sign that Clean Energy Fuels could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Clean Energy Fuels boasts net cash, so it’s fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Clean Energy Fuels’s ability to maintain a healthy balance sheet going forward.

In the last year Clean Energy Fuels wasn’t profitable at an EBIT level, but managed to grow its revenue by 67%, to US$398m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Clean Energy Fuels?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Clean Energy Fuels lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$2.5m and booked a US$49m accounting loss. Given it only has net cash of US$105.6m, the company may need to raise more capital if it doesn’t reach break-even soon. With very solid revenue growth in the last year, Clean Energy Fuels may be on a path to profitability.