Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies CIRCOR International, Inc. (NYSE:CIR) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is CIRCOR International’s Net Debt?

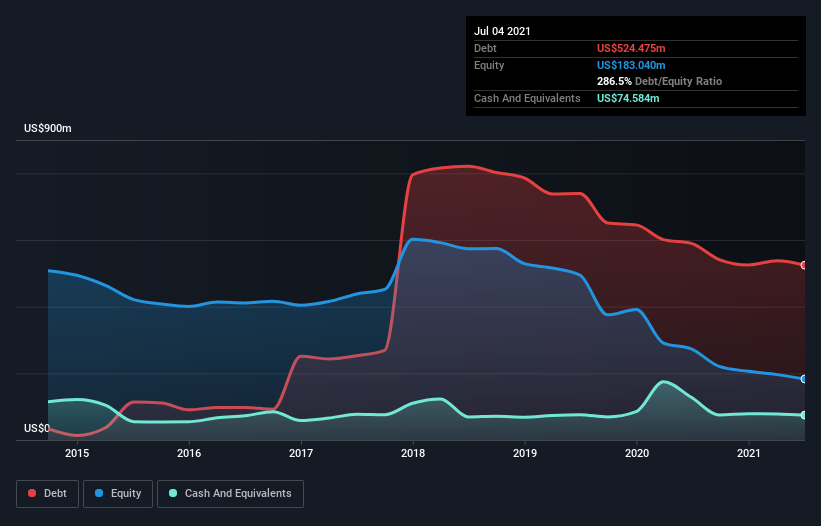

The image below, which you can click on for greater detail, shows that CIRCOR International had debt of US$524.5m at the end of July 2021, a reduction from US$589.9m over a year. However, it does have US$74.6m in cash offsetting this, leading to net debt of about US$449.9m.

How Healthy Is CIRCOR International’s Balance Sheet?

We can see from the most recent balance sheet that CIRCOR International had liabilities of US$170.2m falling due within a year, and liabilities of US$748.7m due beyond that. Offsetting this, it had US$74.6m in cash and US$172.8m in receivables that were due within 12 months. So it has liabilities totalling US$671.6m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company’s US$668.5m market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While CIRCOR International’s debt to EBITDA ratio (5.0) suggests that it uses some debt, its interest cover is very weak, at 0.72, suggesting high leverage. In large part that’s due to the company’s significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Worse, CIRCOR International’s EBIT was down 40% over the last year. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine CIRCOR International’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, CIRCOR International recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

To be frank both CIRCOR International’s interest cover and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. And even its conversion of EBIT to free cash flow fails to inspire much confidence. Taking into account all the aforementioned factors, it looks like CIRCOR International has too much debt. While some investors love that sort of risky play, it’s certainly not our cup of tea.