The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Caleres, Inc. (NYSE:CAL) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Caleres’s Debt?

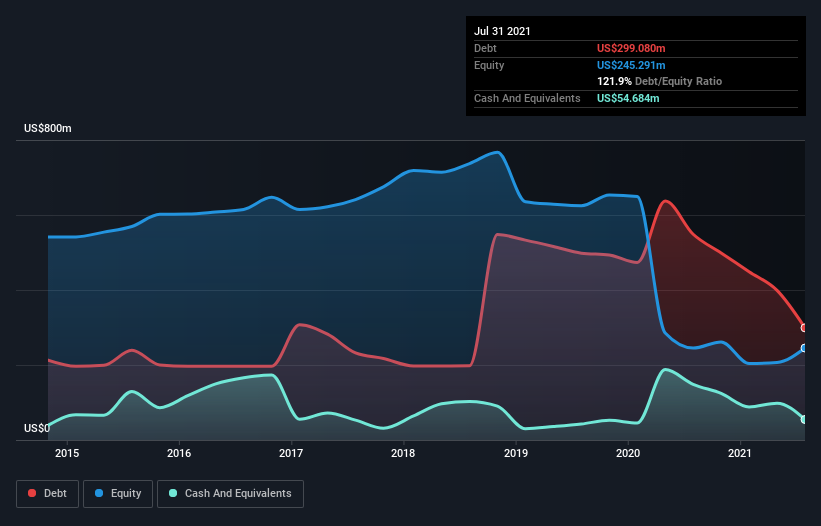

You can click the graphic below for the historical numbers, but it shows that Caleres had US$299.1m of debt in July 2021, down from US$548.6m, one year before. On the flip side, it has US$54.7m in cash leading to net debt of about US$244.4m.

A Look At Caleres’ Liabilities

Zooming in on the latest balance sheet data, we can see that Caleres had liabilities of US$978.7m due within 12 months and liabilities of US$608.9m due beyond that. Offsetting these obligations, it had cash of US$54.7m as well as receivables valued at US$145.5m due within 12 months. So it has liabilities totalling US$1.39b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$873.3m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Caleres would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Looking at its net debt to EBITDA of 1.4 and interest cover of 2.6 times, it seems to us that Caleres is probably using debt in a pretty reasonable way. So we’d recommend keeping a close eye on the impact financing costs are having on the business. Notably, Caleres made a loss at the EBIT level, last year, but improved that to positive EBIT of US$130m in the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Caleres’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Happily for any shareholders, Caleres actually produced more free cash flow than EBIT over the last year. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

We’d go so far as to say Caleres’s level of total liabilities was disappointing. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Caleres’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt.