The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Babcock & Wilcox Enterprises, Inc. (NYSE:BW) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Babcock & Wilcox Enterprises Carry?

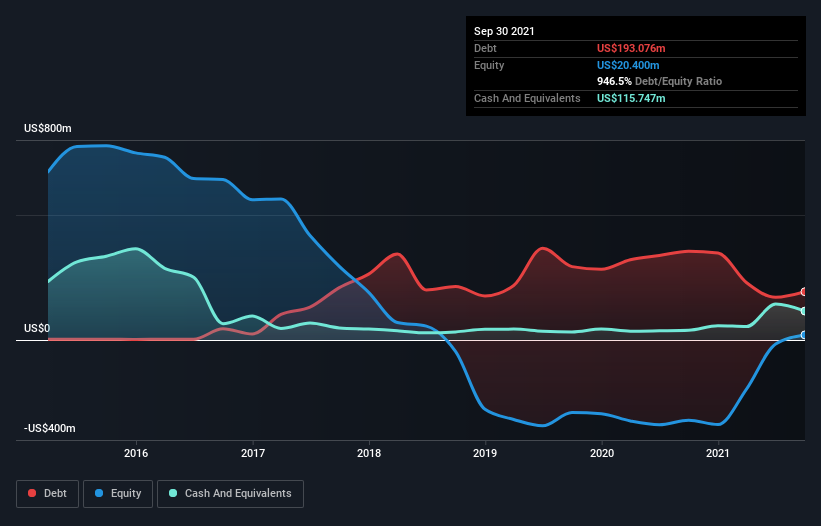

You can click the graphic below for the historical numbers, but it shows that Babcock & Wilcox Enterprises had US$193.1m of debt in September 2021, down from US$355.2m, one year before. However, it also had US$115.7m in cash, and so its net debt is US$77.3m.

A Look At Babcock & Wilcox Enterprises’ Liabilities

According to the last reported balance sheet, Babcock & Wilcox Enterprises had liabilities of US$230.3m due within 12 months, and liabilities of US$478.6m due beyond 12 months. Offsetting these obligations, it had cash of US$115.7m as well as receivables valued at US$235.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$358.1m.

Babcock & Wilcox Enterprises has a market capitalization of US$746.2m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Given net debt is only 1.2 times EBITDA, it is initially surprising to see that Babcock & Wilcox Enterprises’s EBIT has low interest coverage of 1.2 times. So one way or the other, it’s clear the debt levels are not trivial. Pleasingly, Babcock & Wilcox Enterprises is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 128% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Babcock & Wilcox Enterprises’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last two years, Babcock & Wilcox Enterprises saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Babcock & Wilcox Enterprises’s conversion of EBIT to free cash flow and interest cover definitely weigh on it, in our esteem. But the good news is it seems to be able to grow its EBIT with ease. Taking the abovementioned factors together we do think Babcock & Wilcox Enterprises’s debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now.