Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, AT&T Inc. (NYSE:T) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does AT&T Carry?

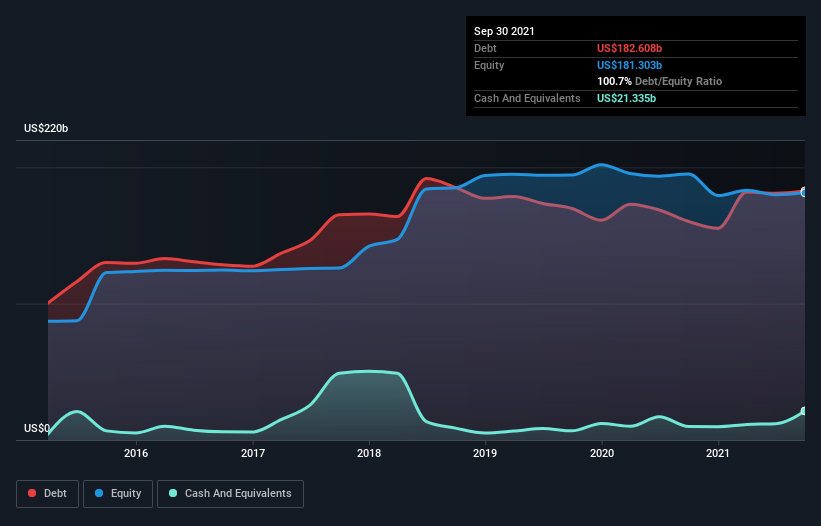

You can click the graphic below for the historical numbers, but it shows that as of September 2021 AT&T had US$182.6b of debt, an increase on US$160.2b, over one year. However, because it has a cash reserve of US$21.3b, its net debt is less, at about US$161.3b.

How Healthy Is AT&T’s Balance Sheet?

According to the last reported balance sheet, AT&T had liabilities of US$81.6b due within 12 months, and liabilities of US$284.2b due beyond 12 months. Offsetting this, it had US$21.3b in cash and US$20.4b in receivables that were due within 12 months. So its liabilities total US$324.1b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$191.4b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, AT&T would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

AT&T’s debt is 3.0 times its EBITDA, and its EBIT cover its interest expense 4.5 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. We saw AT&T grow its EBIT by 8.7% in the last twelve months. Whilst that hardly knocks our socks off it is a positive when it comes to debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if AT&T can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, AT&T recorded free cash flow worth a fulsome 92% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Our View

Neither AT&T’s ability to handle its total liabilities nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. Taking the abovementioned factors together we do think AT&T’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here.