David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Albany International Corp. (NYSE:AIN) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Albany International Carry?

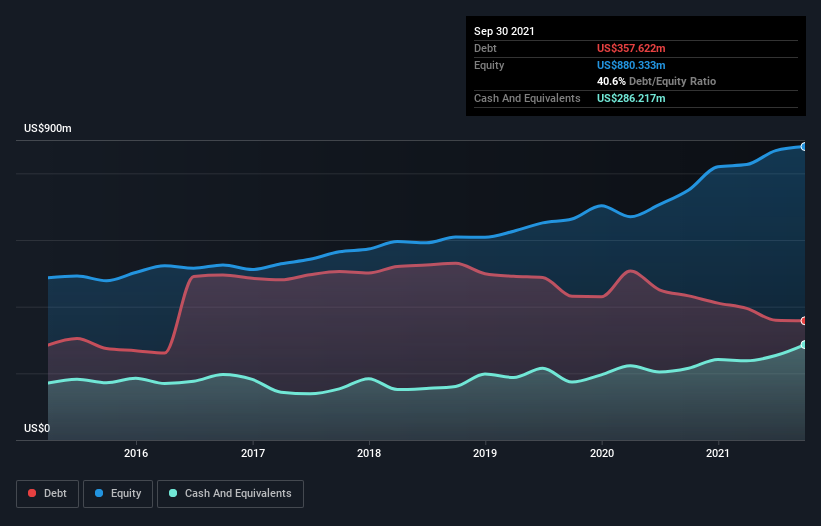

As you can see below, Albany International had US$357.6m of debt at September 2021, down from US$432.4m a year prior. However, because it has a cash reserve of US$286.2m, its net debt is less, at about US$71.4m.

How Strong Is Albany International’s Balance Sheet?

The latest balance sheet data shows that Albany International had liabilities of US$181.5m due within a year, and liabilities of US$478.4m falling due after that. On the other hand, it had cash of US$286.2m and US$315.0m worth of receivables due within a year. So its liabilities total US$58.6m more than the combination of its cash and short-term receivables.

Given Albany International has a market capitalization of US$2.75b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Albany International has a low net debt to EBITDA ratio of only 0.29. And its EBIT easily covers its interest expense, being 11.5 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. But the other side of the story is that Albany International saw its EBIT decline by 3.0% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Albany International’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Albany International recorded free cash flow worth 73% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Albany International’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But truth be told we feel its EBIT growth rate does undermine this impression a bit. Zooming out, Albany International seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity.