Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Abbott Laboratories (NYSE:ABT) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Abbott Laboratories Carry?

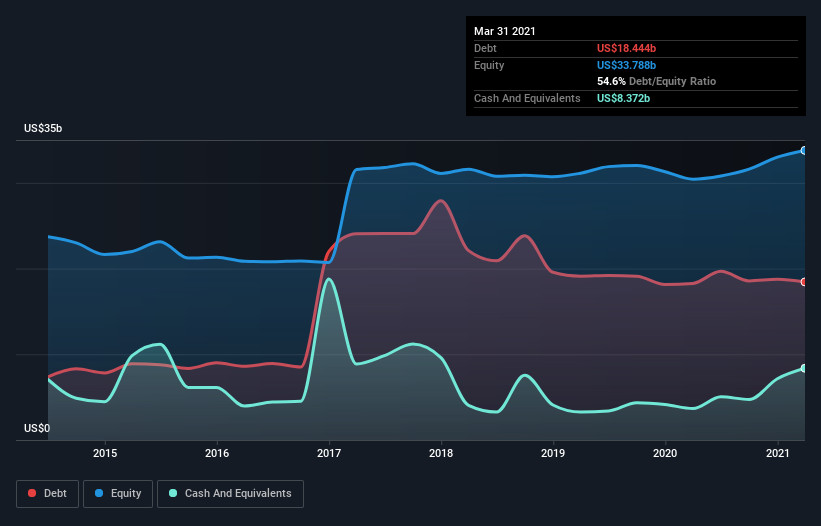

You can click the graphic below for the historical numbers, but it shows that Abbott Laboratories had US$17.3b of debt in March 2021, down from US$18.3b, one year before. However, it also had US$8.37b in cash, and so its net debt is US$8.93b.

A Look At Abbott Laboratories’ Liabilities

According to the last reported balance sheet, Abbott Laboratories had liabilities of US$12.5b due within 12 months, and liabilities of US$26.5b due beyond 12 months. Offsetting these obligations, it had cash of US$8.37b as well as receivables valued at US$6.10b due within 12 months. So its liabilities total US$24.5b more than the combination of its cash and short-term receivables.

Of course, Abbott Laboratories has a titanic market capitalization of US$208.1b, so these liabilities are probably manageable. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Abbott Laboratories’s net debt is only 0.86 times its EBITDA. And its EBIT covers its interest expense a whopping 13.8 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. In addition to that, we’re happy to report that Abbott Laboratories has boosted its EBIT by 43%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Abbott Laboratories’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Abbott Laboratories actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Happily, Abbott Laboratories’s impressive interest cover implies it has the upper hand on its debt. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! We would also note that Medical Equipment industry companies like Abbott Laboratories commonly do use debt without problems. It looks Abbott Laboratories has no trouble standing on its own two feet, and it has no reason to fear its lenders. To our minds it has a healthy happy balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.