David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, The Interpublic Group of Companies, Inc. (NYSE:IPG) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Interpublic Group of Companies’s Net Debt?

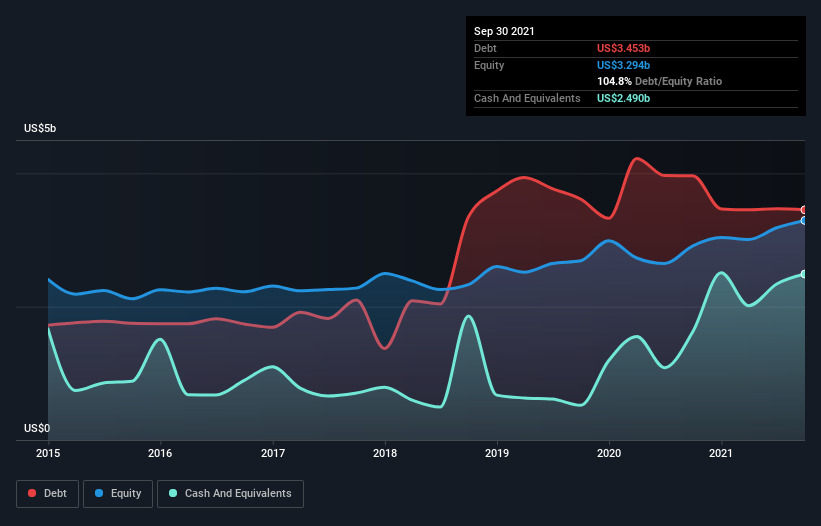

The image below, which you can click on for greater detail, shows that Interpublic Group of Companies had debt of US$3.45b at the end of September 2021, a reduction from US$3.96b over a year. However, because it has a cash reserve of US$2.49b, its net debt is less, at about US$962.8m.

How Strong Is Interpublic Group of Companies’ Balance Sheet?

The latest balance sheet data shows that Interpublic Group of Companies had liabilities of US$9.05b due within a year, and liabilities of US$5.46b falling due after that. On the other hand, it had cash of US$2.49b and US$6.19b worth of receivables due within a year. So its liabilities total US$5.83b more than the combination of its cash and short-term receivables.

Interpublic Group of Companies has a very large market capitalization of US$14.6b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Interpublic Group of Companies has net debt of just 0.55 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 9.5 times, which is more than adequate. On top of that, Interpublic Group of Companies grew its EBIT by 43% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Interpublic Group of Companies can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Interpublic Group of Companies actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Happily, Interpublic Group of Companies’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And the good news does not stop there, as its EBIT growth rate also supports that impression! Zooming out, Interpublic Group of Companies seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. The balance sheet is clearly the area to focus on when you are analysing debt.