Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Intel Corporation (NASDAQ:INTC) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Intel Carry?

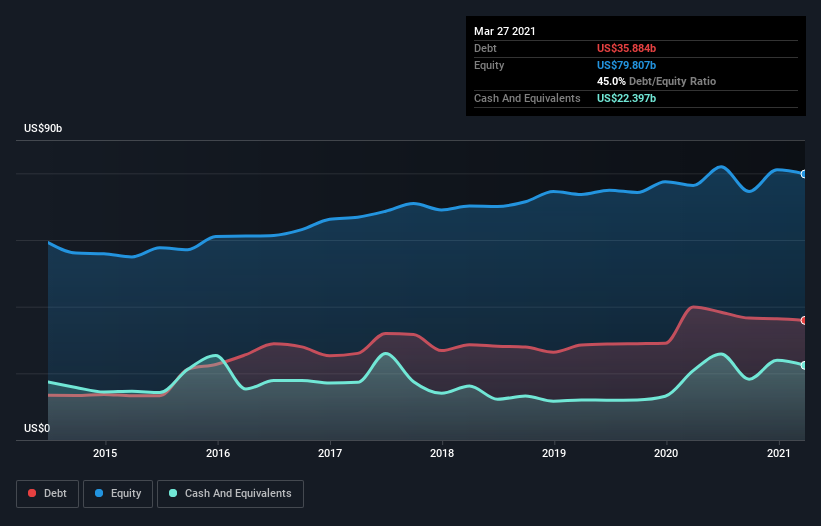

You can click the graphic below for the historical numbers, but it shows that Intel had US$35.4b of debt in March 2021, down from US$39.9b, one year before. However, because it has a cash reserve of US$22.4b, its net debt is less, at about US$13.0b.

How Strong Is Intel’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Intel had liabilities of US$24.2b due within 12 months and liabilities of US$46.7b due beyond that. On the other hand, it had cash of US$22.4b and US$7.42b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$41.0b.

Of course, Intel has a titanic market capitalization of US$233.1b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Intel’s net debt is only 0.37 times its EBITDA. And its EBIT easily covers its interest expense, being 48.2 times the size. So we’re pretty relaxed about its super-conservative use of debt. But the bad news is that Intel has seen its EBIT plunge 11% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Intel’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Intel recorded free cash flow worth 70% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Intel’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But we must concede we find its EBIT growth rate has the opposite effect. All these things considered, it appears that Intel can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.