Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Hyster-Yale Materials Handling, Inc. (NYSE:HY) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Hyster-Yale Materials Handling’s Debt?

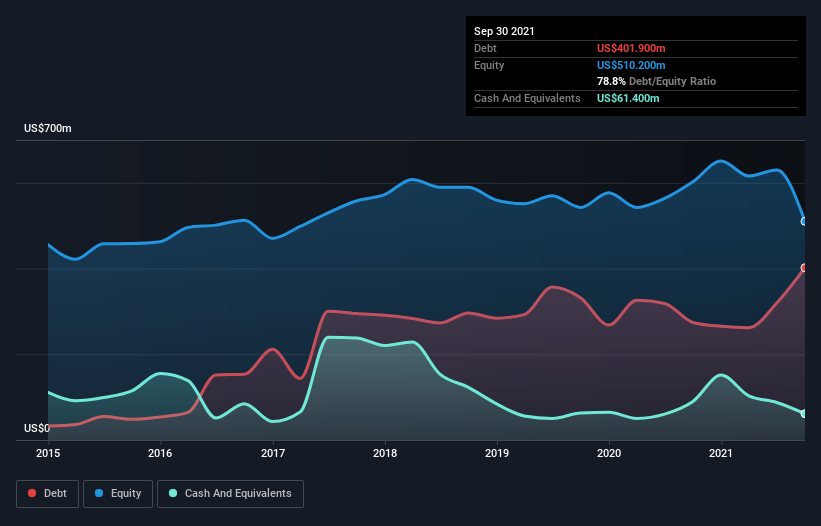

The image below, which you can click on for greater detail, shows that at September 2021 Hyster-Yale Materials Handling had debt of US$401.9m, up from US$274.3m in one year. However, it does have US$61.4m in cash offsetting this, leading to net debt of about US$340.5m.

How Healthy Is Hyster-Yale Materials Handling’s Balance Sheet?

The latest balance sheet data shows that Hyster-Yale Materials Handling had liabilities of US$1.01b due within a year, and liabilities of US$495.1m falling due after that. On the other hand, it had cash of US$61.4m and US$475.8m worth of receivables due within a year. So it has liabilities totalling US$963.5m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$611.8m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. After all, Hyster-Yale Materials Handling would likely require a major re-capitalisation if it had to pay its creditors today. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Hyster-Yale Materials Handling’s ability to maintain a healthy balance sheet going forward.

In the last year Hyster-Yale Materials Handling’s revenue was pretty flat, and it made a negative EBIT. While that hardly impresses, its not too bad either.

Caveat Emptor

Over the last twelve months Hyster-Yale Materials Handling produced an earnings before interest and tax (EBIT) loss. Indeed, it lost US$30m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through US$145m in negative free cash flow over the last year. So suffice it to say we consider the stock to be risky. There’s no doubt that we learn most about debt from the balance sheet.