David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Hologic, Inc. (NASDAQ:HOLX) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

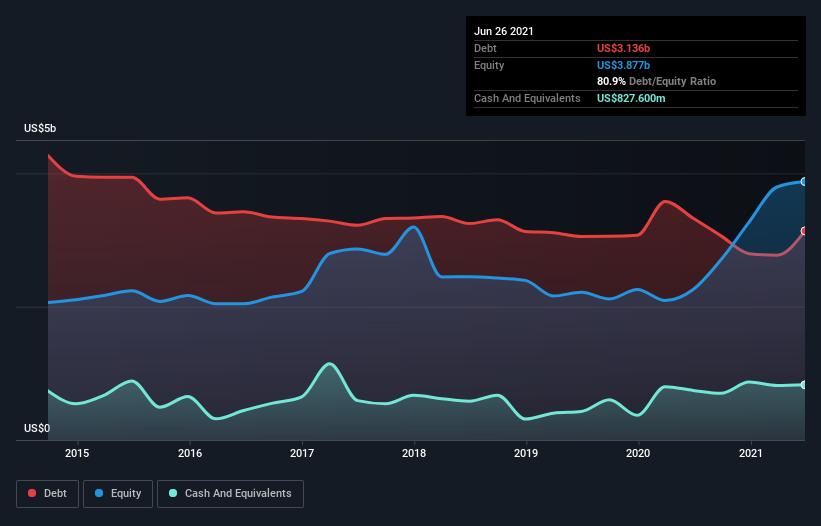

What Is Hologic’s Debt?

As you can see below, Hologic had US$3.14b of debt at June 2021, down from US$3.33b a year prior. On the flip side, it has US$827.6m in cash leading to net debt of about US$2.31b.

A Look At Hologic’s Liabilities

According to the last reported balance sheet, Hologic had liabilities of US$1.46b due within 12 months, and liabilities of US$3.25b due beyond 12 months. Offsetting this, it had US$827.6m in cash and US$943.2m in receivables that were due within 12 months. So its liabilities total US$2.94b more than the combination of its cash and short-term receivables.

Of course, Hologic has a titanic market capitalization of US$20.3b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Hologic’s net debt is only 0.75 times its EBITDA. And its EBIT covers its interest expense a whopping 28.5 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Better yet, Hologic grew its EBIT by 301% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Hologic’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Hologic generated free cash flow amounting to a very robust 82% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, Hologic’s impressive interest cover implies it has the upper hand on its debt. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! It’s also worth noting that Hologic is in the Medical Equipment industry, which is often considered to be quite defensive. We think Hologic is no more beholden to its lenders, than the birds are to birdwatchers. To our minds it has a healthy happy balance sheet. There’s no doubt that we learn most about debt from the balance sheet.