Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, WEC Energy Group, Inc. (NYSE:WEC) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is WEC Energy Group’s Net Debt?

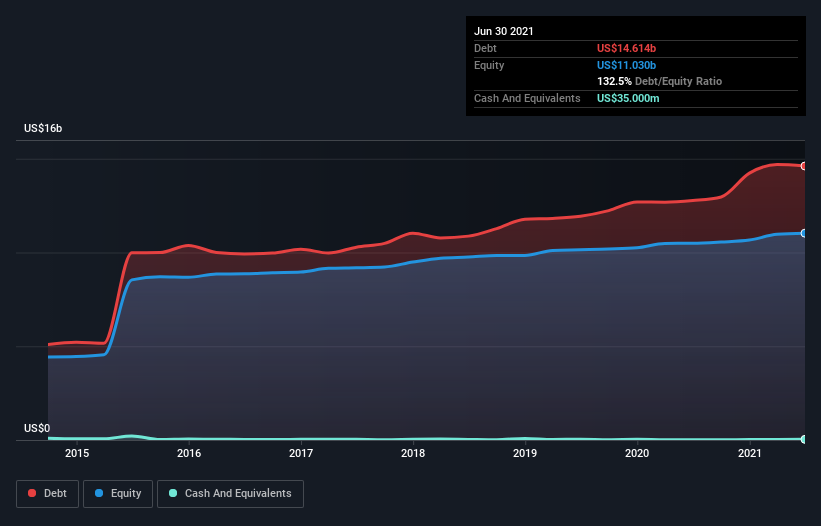

The image below, which you can click on for greater detail, shows that at June 2021 WEC Energy Group had debt of US$14.5b, up from US$12.8b in one year. And it doesn’t have much cash, so its net debt is about the same.

How Strong Is WEC Energy Group’s Balance Sheet?

According to the last reported balance sheet, WEC Energy Group had liabilities of US$3.37b due within 12 months, and liabilities of US$23.4b due beyond 12 months. Offsetting this, it had US$35.0m in cash and US$1.18b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$25.5b.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$30.2b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

WEC Energy Group has a rather high debt to EBITDA ratio of 5.1 which suggests a meaningful debt load. However, its interest coverage of 3.7 is reasonably strong, which is a good sign. Fortunately, WEC Energy Group grew its EBIT by 6.3% in the last year, slowly shrinking its debt relative to earnings. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if WEC Energy Group can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, WEC Energy Group actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

On the face of it, WEC Energy Group’s conversion of EBIT to free cash flow left us tentative about the stock, and its net debt to EBITDA was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. We should also note that Integrated Utilities industry companies like WEC Energy Group commonly do use debt without problems. Overall, we think it’s fair to say that WEC Energy Group has enough debt that there are some real risks around the balance sheet. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There’s no doubt that we learn most about debt from the balance sheet.