Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Terex Corporation (NYSE:TEX) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Terex Carry?

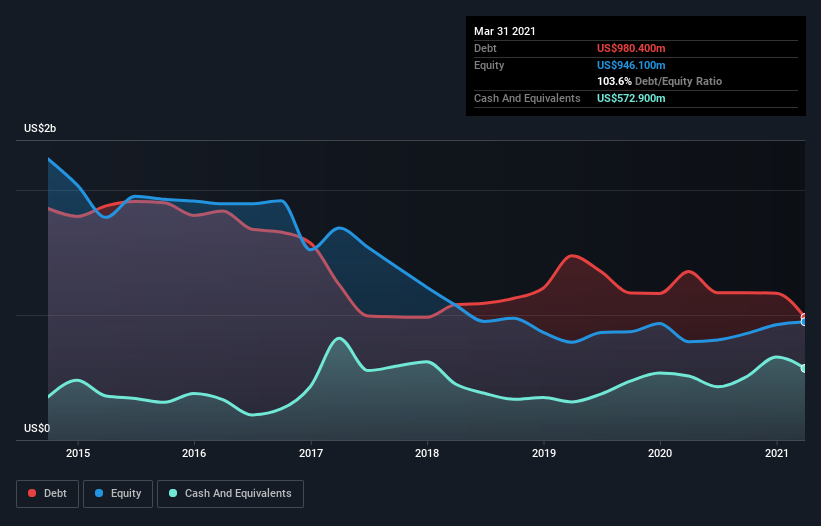

As you can see below, Terex had US$868.3m of debt at March 2021, down from US$1.35b a year prior. However, because it has a cash reserve of US$572.9m, its net debt is less, at about US$295.4m.

A Look At Terex’s Liabilities

We can see from the most recent balance sheet that Terex had liabilities of US$838.0m falling due within a year, and liabilities of US$1.18b due beyond that. On the other hand, it had cash of US$572.9m and US$488.3m worth of receivables due within a year. So it has liabilities totalling US$958.2m more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Terex is worth US$3.14b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Even though Terex’s debt is only 1.5, its interest cover is really very low at 2.4. This does suggest the company is paying fairly high interest rates. Either way there’s no doubt the stock is using meaningful leverage. Shareholders should be aware that Terex’s EBIT was down 38% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Terex’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Terex recorded free cash flow worth 58% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Terex’s struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. But on the bright side, its ability to to convert EBIT to free cash flow isn’t too shabby at all. Taking the abovementioned factors together we do think Terex’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.