Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Howmet Aerospace Inc. (NYSE:HWM) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Howmet Aerospace’s Debt?

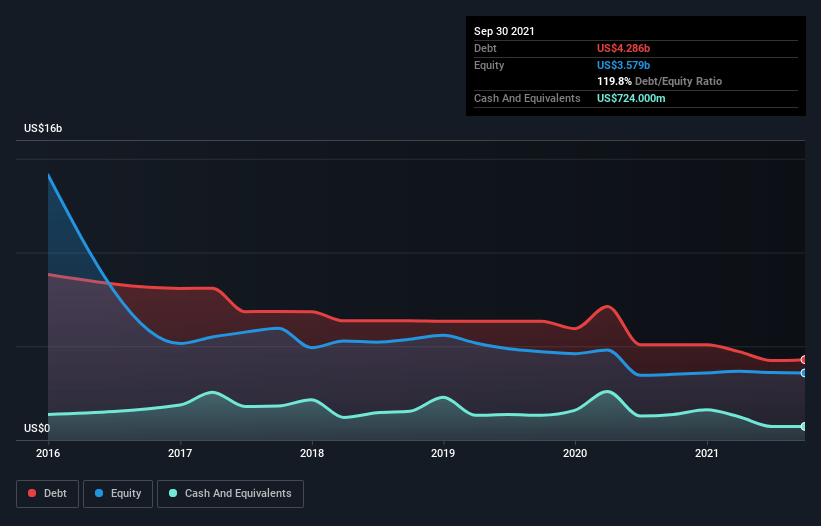

You can click the graphic below for the historical numbers, but it shows that Howmet Aerospace had US$4.29b of debt in September 2021, down from US$5.08b, one year before. However, because it has a cash reserve of US$724.0m, its net debt is less, at about US$3.56b.

How Strong Is Howmet Aerospace’s Balance Sheet?

According to the last reported balance sheet, Howmet Aerospace had liabilities of US$1.21b due within 12 months, and liabilities of US$5.57b due beyond 12 months. Offsetting this, it had US$724.0m in cash and US$465.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$5.59b.

While this might seem like a lot, it is not so bad since Howmet Aerospace has a huge market capitalization of US$14.3b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn’t worry about Howmet Aerospace’s net debt to EBITDA ratio of 2.9, we think its super-low interest cover of 2.5 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Notably, Howmet Aerospace’s EBIT was pretty flat over the last year, which isn’t ideal given the debt load. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Howmet Aerospace can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Considering the last three years, Howmet Aerospace actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

On the face of it, Howmet Aerospace’s interest cover left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to grow its EBIT isn’t such a worry. Once we consider all the factors above, together, it seems to us that Howmet Aerospace’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt.