The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Comstock Resources, Inc. (NYSE:CRK) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

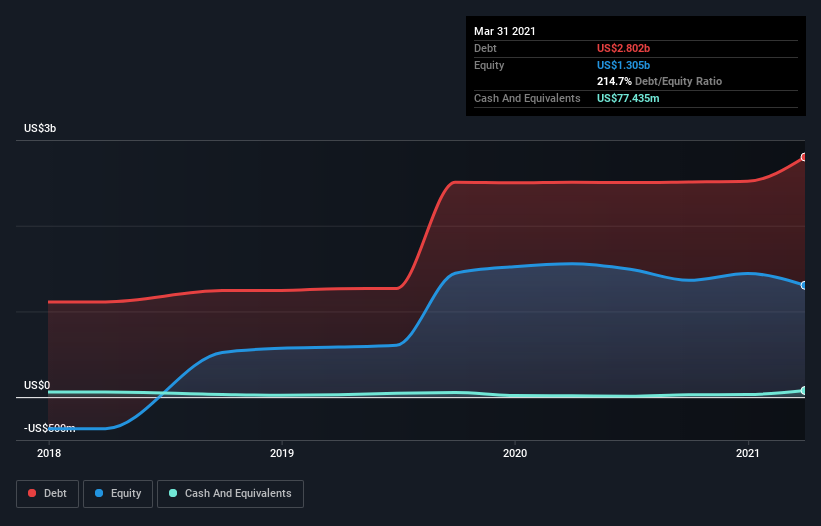

What Is Comstock Resources’s Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Comstock Resources had US$2.80b of debt, an increase on US$2.51b, over one year. However, it also had US$77.4m in cash, and so its net debt is US$2.72b.

How Healthy Is Comstock Resources’ Balance Sheet?

According to the last reported balance sheet, Comstock Resources had liabilities of US$433.6m due within 12 months, and liabilities of US$3.00b due beyond 12 months. Offsetting this, it had US$77.4m in cash and US$152.8m in receivables that were due within 12 months. So its liabilities total US$3.20b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$1.37b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. After all, Comstock Resources would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn’t worry about Comstock Resources’s net debt to EBITDA ratio of 3.9, we think its super-low interest cover of 1.1 times is a sign of high leverage. In large part that’s due to the company’s significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Fortunately, Comstock Resources grew its EBIT by 4.9% in the last year, slowly shrinking its debt relative to earnings. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Comstock Resources’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, Comstock Resources actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

To be frank both Comstock Resources’s interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. Taking into account all the aforementioned factors, it looks like Comstock Resources has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. While Comstock Resources didn’t make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away.