David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Carrier Global Corporation (NYSE:CARR) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Carrier Global Carry?

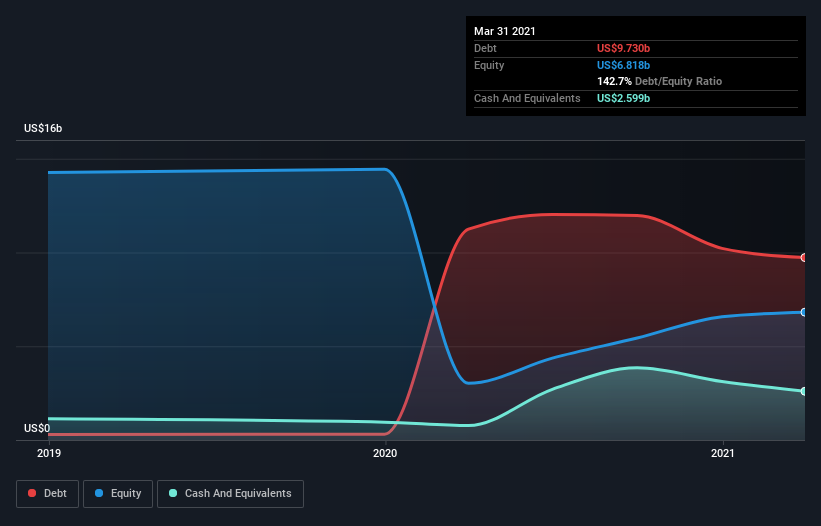

You can click the graphic below for the historical numbers, but it shows that Carrier Global had US$9.57b of debt in March 2021, down from US$11.2b, one year before. However, because it has a cash reserve of US$2.60b, its net debt is less, at about US$6.97b.

A Look At Carrier Global’s Liabilities

The latest balance sheet data shows that Carrier Global had liabilities of US$5.14b due within a year, and liabilities of US$12.9b falling due after that. Offsetting this, it had US$2.60b in cash and US$3.53b in receivables that were due within 12 months. So its liabilities total US$11.9b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Carrier Global is worth a massive US$39.9b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Carrier Global’s debt is 2.8 times its EBITDA, and its EBIT cover its interest expense 6.2 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Unfortunately, Carrier Global’s EBIT flopped 16% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Carrier Global can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Carrier Global produced sturdy free cash flow equating to 71% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Carrier Global’s struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. In particular, its conversion of EBIT to free cash flow was re-invigorating. Looking at all the angles mentioned above, it does seem to us that Carrier Global is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There’s no doubt that we learn most about debt from the balance sheet.