The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Avista Corporation (NYSE:AVA) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Avista Carry?

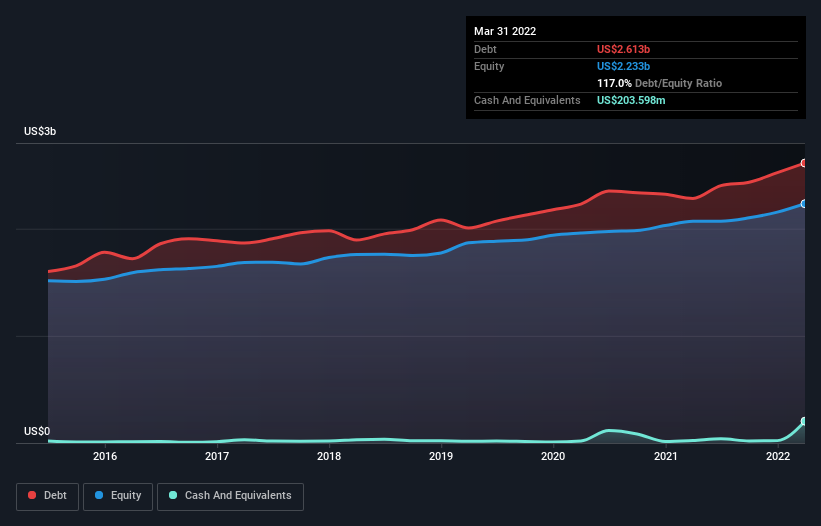

You can click the graphic below for the historical numbers, but it shows that as of March 2022 Avista had US$2.61b of debt, an increase on US$2.28b, over one year. However, it also had US$203.6m in cash, and so its net debt is US$2.41b.

How Strong Is Avista’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Avista had liabilities of US$641.9m due within 12 months and liabilities of US$4.16b due beyond that. On the other hand, it had cash of US$203.6m and US$227.6m worth of receivables due within a year. So it has liabilities totalling US$4.37b more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company’s US$3.09b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Avista shareholders face the double whammy of a high net debt to EBITDA ratio (5.4), and fairly weak interest coverage, since EBIT is just 2.1 times the interest expense. The debt burden here is substantial. Another concern for investors might be that Avista’s EBIT fell 15% in the last year. If that’s the way things keep going handling the debt load will be like delivering hot coffees on a pogo stick. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Avista’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Avista burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, Avista’s level of total liabilities left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. And furthermore, its interest cover also fails to instill confidence. It’s also worth noting that Avista is in the Integrated Utilities industry, which is often considered to be quite defensive. We think the chances that Avista has too much debt a very significant. To us, that makes the stock rather risky, like walking through a dog park with your eyes closed. But some investors may feel differently.