Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Avaya Holdings Corp. (NYSE:AVYA) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

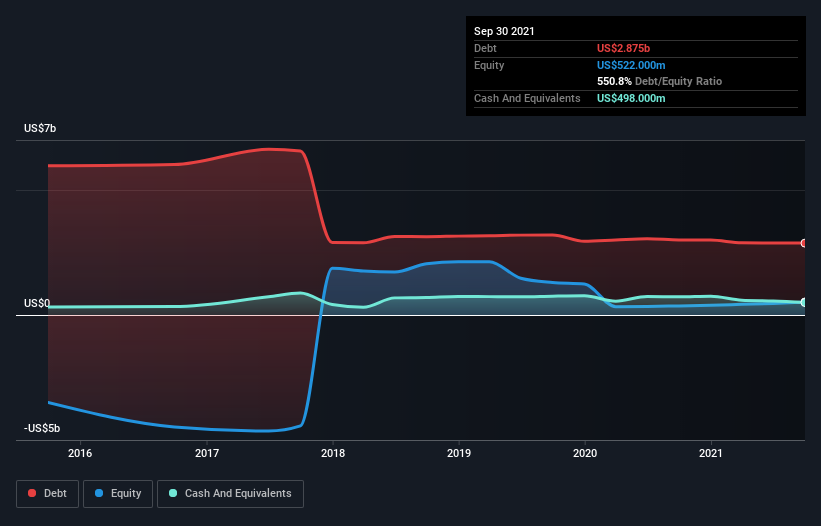

What Is Avaya Holdings’s Debt?

As you can see below, Avaya Holdings had US$2.88b of debt at September 2021, down from US$3.00b a year prior. On the flip side, it has US$498.0m in cash leading to net debt of about US$2.38b.

A Look At Avaya Holdings’ Liabilities

We can see from the most recent balance sheet that Avaya Holdings had liabilities of US$1.10b falling due within a year, and liabilities of US$4.37b due beyond that. Offsetting this, it had US$498.0m in cash and US$825.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.14b.

This deficit casts a shadow over the US$1.70b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. After all, Avaya Holdings would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Avaya Holdings’s debt to EBITDA ratio (5.0) suggests that it uses some debt, its interest cover is very weak, at 1.1, suggesting high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. However, one redeeming factor is that Avaya Holdings grew its EBIT at 14% over the last 12 months, boosting its ability to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Avaya Holdings can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. In the last three years, Avaya Holdings created free cash flow amounting to 15% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

To be frank both Avaya Holdings’s interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it’s pretty decent at growing its EBIT; that’s encouraging. Overall, it seems to us that Avaya Holdings’s balance sheet is really quite a risk to the business. For this reason we’re pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start.