Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Atmos Energy Corporation (NYSE:ATO) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Atmos Energy’s Debt?

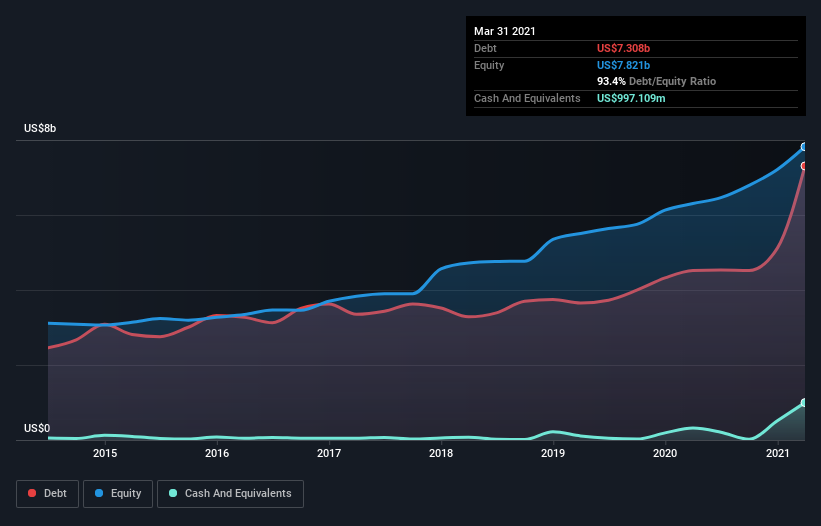

As you can see below, at the end of March 2021, Atmos Energy had US$7.31b of debt, up from US$4.52b a year ago. Click the image for more detail. However, because it has a cash reserve of US$997.1m, its net debt is less, at about US$6.31b.

How Healthy Is Atmos Energy’s Balance Sheet?

The latest balance sheet data shows that Atmos Energy had liabilities of US$871.3m due within a year, and liabilities of US$10.7b falling due after that. Offsetting this, it had US$997.1m in cash and US$469.6m in receivables that were due within 12 months. So it has liabilities totalling US$10.1b more than its cash and near-term receivables, combined.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$13.0b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Atmos Energy has a debt to EBITDA ratio of 4.6, which signals significant debt, but is still pretty reasonable for most types of business. But its EBIT was about 11.4 times its interest expense, implying the company isn’t really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. If Atmos Energy can keep growing EBIT at last year’s rate of 16% over the last year, then it will find its debt load easier to manage. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Atmos Energy’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Atmos Energy burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Atmos Energy’s struggle to convert EBIT to free cash flow had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example its interest cover was refreshing. We should also note that Gas Utilities industry companies like Atmos Energy commonly do use debt without problems. Taking the abovementioned factors together we do think Atmos Energy’s debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.