Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Green Brick Partners, Inc. (NYSE:GRBK) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Green Brick Partners’s Debt?

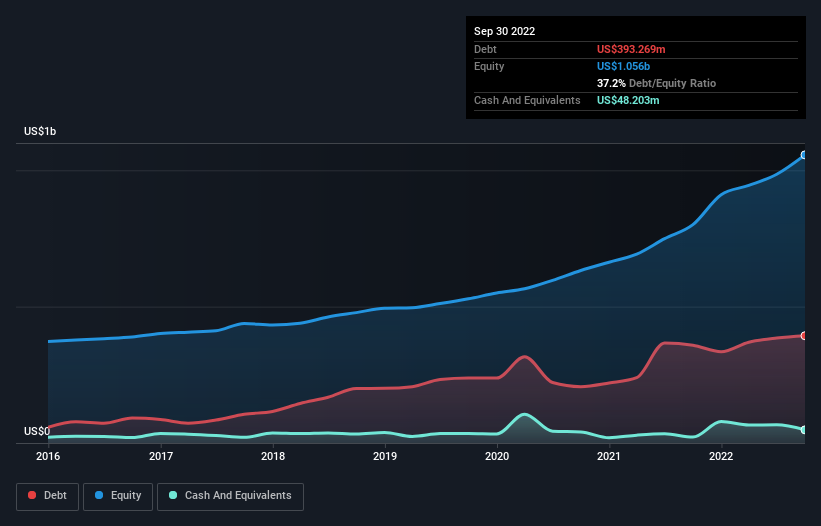

As you can see below, at the end of September 2022, Green Brick Partners had US$393.3m of debt, up from US$358.7m a year ago. Click the image for more detail. On the flip side, it has US$48.2m in cash leading to net debt of about US$345.1m.

How Strong Is Green Brick Partners’ Balance Sheet?

We can see from the most recent balance sheet that Green Brick Partners had liabilities of US$204.5m falling due within a year, and liabilities of US$396.8m due beyond that. On the other hand, it had cash of US$48.2m and US$7.24m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$545.8m.

This deficit isn’t so bad because Green Brick Partners is worth US$1.12b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Green Brick Partners has a low net debt to EBITDA ratio of only 0.94. And its EBIT covers its interest expense a whopping 1k times over. So we’re pretty relaxed about its super-conservative use of debt. On top of that, Green Brick Partners grew its EBIT by 94% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Green Brick Partners can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, Green Brick Partners actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Both Green Brick Partners’s ability to to cover its interest expense with its EBIT and its EBIT growth rate gave us comfort that it can handle its debt. But truth be told its conversion of EBIT to free cash flow had us nibbling our nails. Considering this range of data points, we think Green Brick Partners is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There’s no doubt that we learn most about debt from the balance sheet.