The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Equifax Inc. (NYSE:EFX) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Equifax’s Debt?

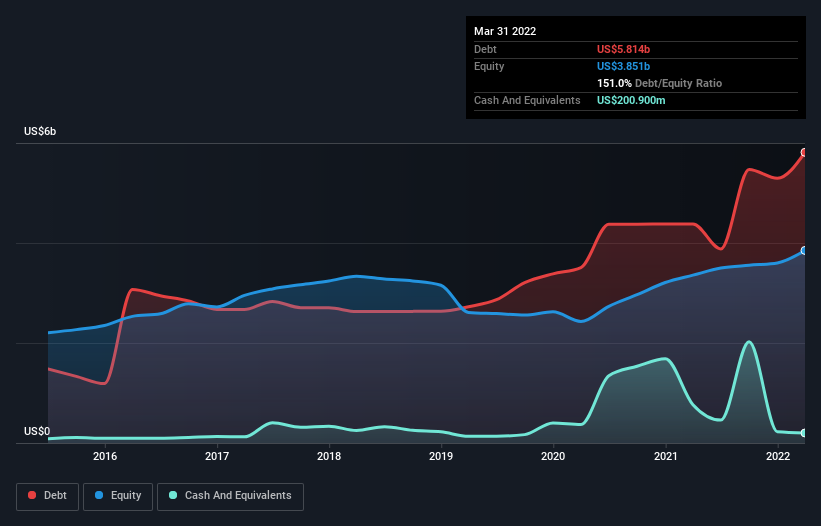

As you can see below, at the end of March 2022, Equifax had US$5.81b of debt, up from US$4.38b a year ago. Click the image for more detail. However, because it has a cash reserve of US$200.9m, its net debt is less, at about US$5.61b.

How Healthy Is Equifax’s Balance Sheet?

We can see from the most recent balance sheet that Equifax had liabilities of US$2.34b falling due within a year, and liabilities of US$5.20b due beyond that. Offsetting these obligations, it had cash of US$200.9m as well as receivables valued at US$856.8m due within 12 months. So it has liabilities totalling US$6.48b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Equifax has a huge market capitalization of US$21.2b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Equifax has net debt to EBITDA of 3.3 suggesting it uses a fair bit of leverage to boost returns. On the plus side, its EBIT was 7.9 times its interest expense, and its net debt to EBITDA, was quite high, at 3.3. Importantly, Equifax grew its EBIT by 35% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Equifax can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Equifax recorded free cash flow of 40% of its EBIT, which is weaker than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On our analysis Equifax’s EBIT growth rate should signal that it won’t have too much trouble with its debt. However, our other observations weren’t so heartening. For example, its net debt to EBITDA makes us a little nervous about its debt. Considering this range of data points, we think Equifax is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There’s no doubt that we learn most about debt from the balance sheet.