Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Enerpac Tool Group Corp. (NYSE:EPAC) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Enerpac Tool Group’s Debt?

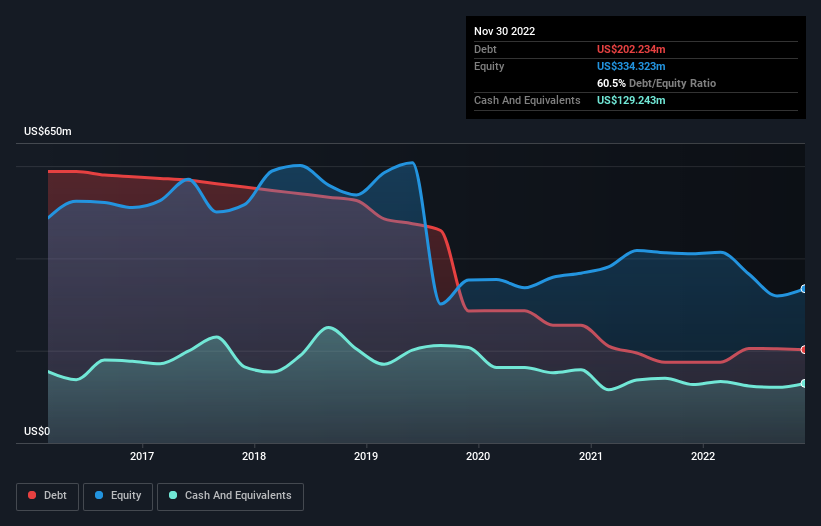

The image below, which you can click on for greater detail, shows that at November 2022 Enerpac Tool Group had debt of US$202.2m, up from US$175.0m in one year. However, because it has a cash reserve of US$129.2m, its net debt is less, at about US$73.0m.

How Healthy Is Enerpac Tool Group’s Balance Sheet?

The latest balance sheet data shows that Enerpac Tool Group had liabilities of US$154.1m due within a year, and liabilities of US$285.9m falling due after that. Offsetting these obligations, it had cash of US$129.2m as well as receivables valued at US$99.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$211.7m.

Of course, Enerpac Tool Group has a market capitalization of US$1.44b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Enerpac Tool Group’s net debt is only 0.84 times its EBITDA. And its EBIT covers its interest expense a whopping 12.3 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Also good is that Enerpac Tool Group grew its EBIT at 17% over the last year, further increasing its ability to manage debt. There’s no doubt that we learn most about debt from the balance sheet. But you can’t view debt in total isolation; since Enerpac Tool Group will need earnings to service that debt. So when considering debt, it’s definitely worth looking at the earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Enerpac Tool Group produced sturdy free cash flow equating to 75% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Enerpac Tool Group’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Zooming out, Enerpac Tool Group seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity.