Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Stepan Company (NYSE:SCL) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Stepan’s Debt?

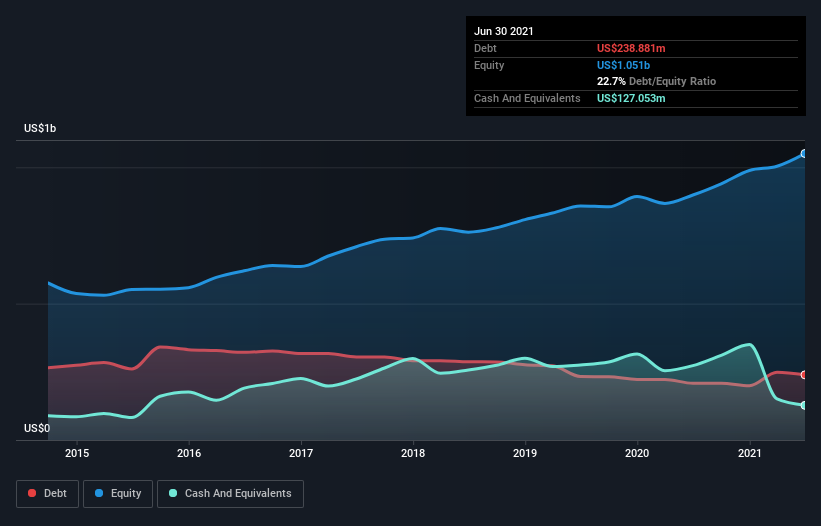

The image below, which you can click on for greater detail, shows that at June 2021 Stepan had debt of US$238.9m, up from US$207.9m in one year. However, it does have US$127.1m in cash offsetting this, leading to net debt of about US$111.8m.

How Healthy Is Stepan’s Balance Sheet?

According to the last reported balance sheet, Stepan had liabilities of US$464.5m due within 12 months, and liabilities of US$372.3m due beyond 12 months. On the other hand, it had cash of US$127.1m and US$391.7m worth of receivables due within a year. So its liabilities total US$318.0m more than the combination of its cash and short-term receivables.

Since publicly traded Stepan shares are worth a total of US$2.50b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Stepan has a low net debt to EBITDA ratio of only 0.42. And its EBIT covers its interest expense a whopping 30.6 times over. So we’re pretty relaxed about its super-conservative use of debt. On top of that, Stepan grew its EBIT by 36% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Stepan’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Stepan produced sturdy free cash flow equating to 53% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Stepan’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Looking at the bigger picture, we think Stepan’s use of debt seems quite reasonable and we’re not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity.