The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Agnico Eagle Mines Limited (NYSE:AEM) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Agnico Eagle Mines’s Net Debt?

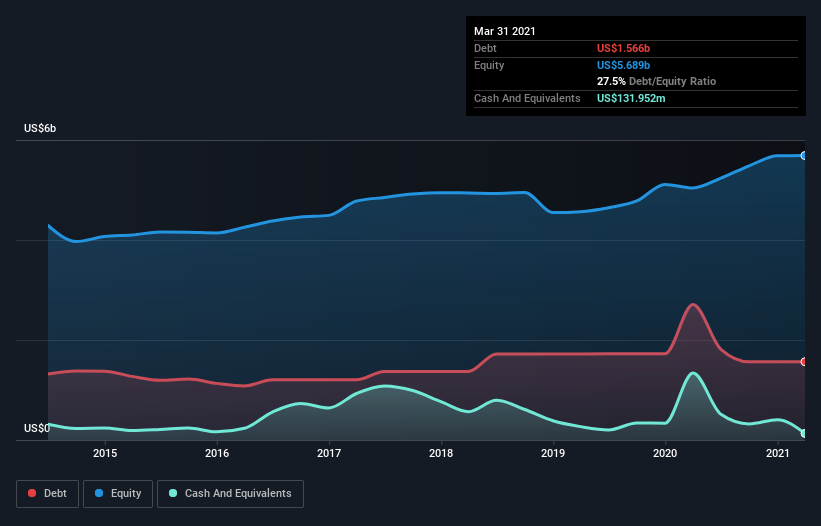

As you can see below, Agnico Eagle Mines had US$1.57b of debt at March 2021, down from US$2.71b a year prior. However, it does have US$132.0m in cash offsetting this, leading to net debt of about US$1.43b.

A Look At Agnico Eagle Mines’ Liabilities

According to the last reported balance sheet, Agnico Eagle Mines had liabilities of US$455.3m due within 12 months, and liabilities of US$3.41b due beyond 12 months. Offsetting these obligations, it had cash of US$132.0m as well as receivables valued at US$88.6m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.64b.

Agnico Eagle Mines has a very large market capitalization of US$15.4b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Agnico Eagle Mines has a low net debt to EBITDA ratio of only 0.80. And its EBIT easily covers its interest expense, being 14.6 times the size. So we’re pretty relaxed about its super-conservative use of debt. On top of that, Agnico Eagle Mines grew its EBIT by 39% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Agnico Eagle Mines can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Agnico Eagle Mines reported free cash flow worth 4.9% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

The good news is that Agnico Eagle Mines’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. All these things considered, it appears that Agnico Eagle Mines can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.