Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Construction Partners, Inc. (NASDAQ:ROAD) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Construction Partners Carry?

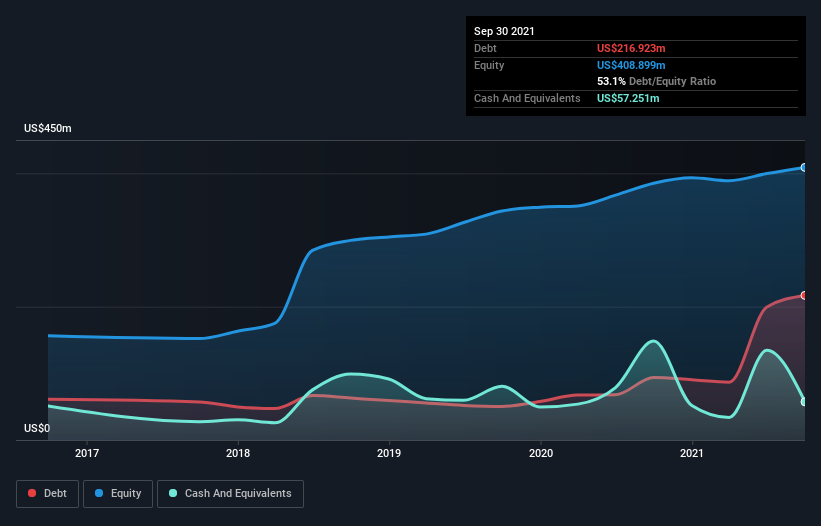

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Construction Partners had US$216.9m of debt, an increase on US$93.8m, over one year. On the flip side, it has US$57.3m in cash leading to net debt of about US$159.7m.

A Look At Construction Partners’ Liabilities

Zooming in on the latest balance sheet data, we can see that Construction Partners had liabilities of US$158.0m due within 12 months and liabilities of US$239.8m due beyond that. On the other hand, it had cash of US$57.3m and US$181.4m worth of receivables due within a year. So it has liabilities totalling US$159.1m more than its cash and near-term receivables, combined.

Since publicly traded Construction Partners shares are worth a total of US$1.57b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Construction Partners’s net debt to EBITDA ratio of about 2.0 suggests only moderate use of debt. And its commanding EBIT of 13.2 times its interest expense, implies the debt load is as light as a peacock feather. Shareholders should be aware that Construction Partners’s EBIT was down 43% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Construction Partners’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Construction Partners recorded free cash flow of 32% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Neither Construction Partners’s ability to grow its EBIT nor its conversion of EBIT to free cash flow gave us confidence in its ability to take on more debt. But the good news is it seems to be able to cover its interest expense with its EBIT with ease. We think that Construction Partners’s debt does make it a bit risky, after considering the aforementioned data points together. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.