Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Coeur Mining, Inc. (NYSE:CDE) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Coeur Mining’s Net Debt?

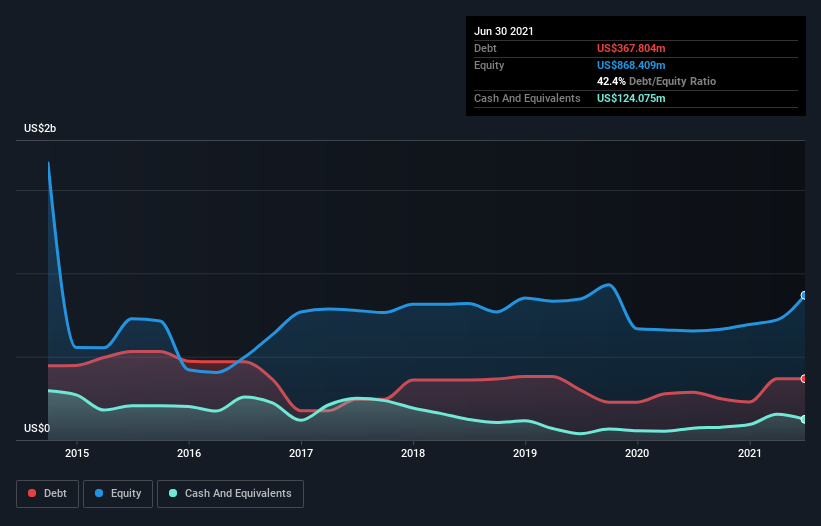

The image below, which you can click on for greater detail, shows that at June 2021 Coeur Mining had debt of US$367.8m, up from US$287.2m in one year. However, it does have US$124.1m in cash offsetting this, leading to net debt of about US$243.7m.

How Strong Is Coeur Mining’s Balance Sheet?

We can see from the most recent balance sheet that Coeur Mining had liabilities of US$227.8m falling due within a year, and liabilities of US$611.8m due beyond that. Offsetting this, it had US$124.1m in cash and US$22.9m in receivables that were due within 12 months. So its liabilities total US$692.7m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Coeur Mining has a market capitalization of US$1.64b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Coeur Mining has net debt of just 0.82 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 7.8 times, which is more than adequate. It was also good to see that despite losing money on the EBIT line last year, Coeur Mining turned things around in the last 12 months, delivering and EBIT of US$154m. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Coeur Mining can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. In the last year, Coeur Mining basically broke even on a free cash flow basis. Some might say that’s a concern, when it comes considering how easily it would be for it to down debt.

Our View

Coeur Mining’s conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to handle its debt, based on its EBITDA, isn’t too shabby at all. We think that Coeur Mining’s debt does make it a bit risky, after considering the aforementioned data points together. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of.