Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Catalent, Inc. (NYSE:CTLT) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Catalent’s Debt?

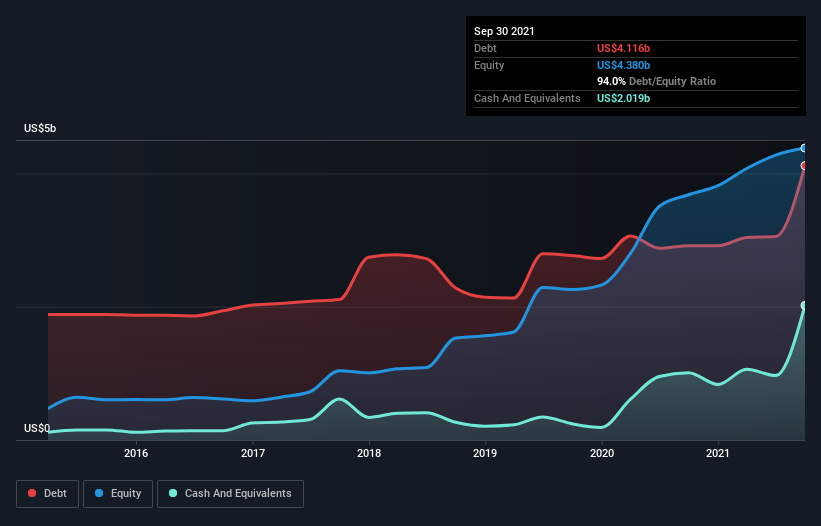

The image below, which you can click on for greater detail, shows that at September 2021 Catalent had debt of US$4.12b, up from US$2.91b in one year. On the flip side, it has US$2.02b in cash leading to net debt of about US$2.10b.

A Look At Catalent’s Liabilities

According to the last reported balance sheet, Catalent had liabilities of US$1.10b due within 12 months, and liabilities of US$4.71b due beyond 12 months. Offsetting these obligations, it had cash of US$2.02b as well as receivables valued at US$1.06b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.73b.

Since publicly traded Catalent shares are worth a very impressive total of US$16.6b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Catalent has net debt worth 2.0 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 6.6 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. It is well worth noting that Catalent’s EBIT shot up like bamboo after rain, gaining 59% in the last twelve months. That’ll make it easier to manage its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Catalent’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Catalent recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

When it comes to the balance sheet, the standout positive for Catalent was the fact that it seems able to grow its EBIT confidently. However, our other observations weren’t so heartening. In particular, conversion of EBIT to free cash flow gives us cold feet. When we consider all the factors mentioned above, we do feel a bit cautious about Catalent’s use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky.