David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, BWX Technologies, Inc. (NYSE:BWXT) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does BWX Technologies Carry?

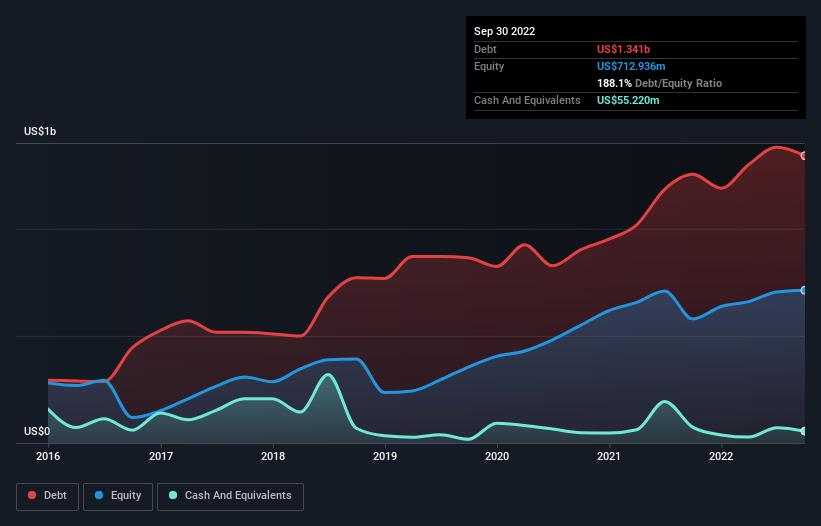

You can click the graphic below for the historical numbers, but it shows that as of September 2022 BWX Technologies had US$1.34b of debt, an increase on US$1.25b, over one year. On the flip side, it has US$55.2m in cash leading to net debt of about US$1.29b.

How Strong Is BWX Technologies’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that BWX Technologies had liabilities of US$406.8m due within 12 months and liabilities of US$1.55b due beyond that. On the other hand, it had cash of US$55.2m and US$728.3m worth of receivables due within a year. So it has liabilities totalling US$1.18b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since BWX Technologies has a market capitalization of US$5.50b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

BWX Technologies has a debt to EBITDA ratio of 2.8, which signals significant debt, but is still pretty reasonable for most types of business. However, its interest coverage of 12.5 is very high, suggesting that the interest expense on the debt is currently quite low. If BWX Technologies can keep growing EBIT at last year’s rate of 16% over the last year, then it will find its debt load easier to manage. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if BWX Technologies can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, BWX Technologies created free cash flow amounting to 14% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

On our analysis BWX Technologies’s interest cover should signal that it won’t have too much trouble with its debt. However, our other observations weren’t so heartening. For example, its conversion of EBIT to free cash flow makes us a little nervous about its debt. Considering this range of data points, we think BWX Technologies is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start.