Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Autoliv, Inc. (NYSE:ALV) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Autoliv Carry?

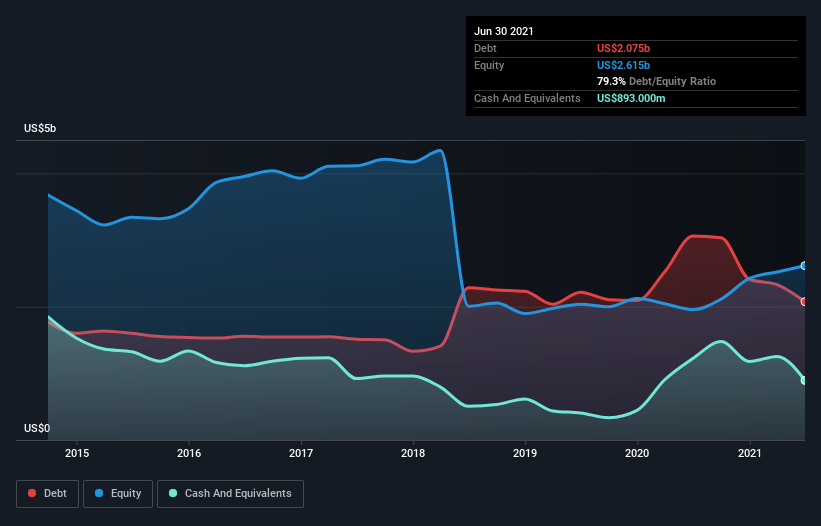

The image below, which you can click on for greater detail, shows that Autoliv had debt of US$2.08b at the end of June 2021, a reduction from US$3.06b over a year. However, it also had US$893.0m in cash, and so its net debt is US$1.18b.

How Healthy Is Autoliv’s Balance Sheet?

According to the last reported balance sheet, Autoliv had liabilities of US$2.85b due within 12 months, and liabilities of US$2.17b due beyond 12 months. On the other hand, it had cash of US$893.0m and US$1.72b worth of receivables due within a year. So its liabilities total US$2.41b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Autoliv has a market capitalization of US$8.01b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Autoliv has a low net debt to EBITDA ratio of only 0.91. And its EBIT covers its interest expense a whopping 13.1 times over. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Autoliv has boosted its EBIT by 57%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Autoliv can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Autoliv’s free cash flow amounted to 44% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Happily, Autoliv’s impressive interest cover implies it has the upper hand on its debt. And the good news does not stop there, as its EBIT growth rate also supports that impression! When we consider the range of factors above, it looks like Autoliv is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start.