David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Applied Materials, Inc. (NASDAQ:AMAT) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Applied Materials’s Debt?

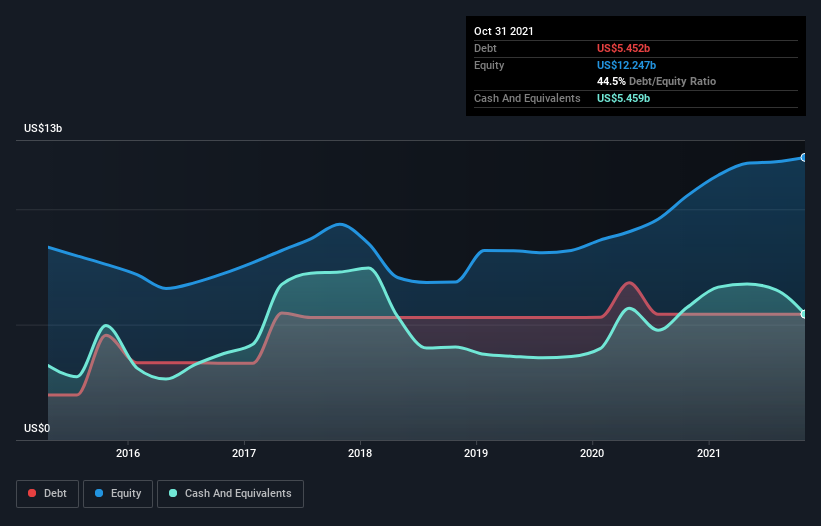

As you can see below, Applied Materials had US$5.45b of debt, at October 2021, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$5.46b in cash, so it actually has US$7.00m net cash.

How Healthy Is Applied Materials’ Balance Sheet?

We can see from the most recent balance sheet that Applied Materials had liabilities of US$6.34b falling due within a year, and liabilities of US$7.23b due beyond that. Offsetting these obligations, it had cash of US$5.46b as well as receivables valued at US$5.15b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.97b.

Given Applied Materials has a humongous market capitalization of US$117.6b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Applied Materials boasts net cash, so it’s fair to say it does not have a heavy debt load!

In addition to that, we’re happy to report that Applied Materials has boosted its EBIT by 62%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Applied Materials’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Applied Materials may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Applied Materials produced sturdy free cash flow equating to 73% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

We could understand if investors are concerned about Applied Materials’s liabilities, but we can be reassured by the fact it has has net cash of US$7.00m. And we liked the look of last year’s 62% year-on-year EBIT growth. So we don’t think Applied Materials’s use of debt is risky. There’s no doubt that we learn most about debt from the balance sheet.