Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Analog Devices, Inc. (NASDAQ:ADI) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Analog Devices Carry?

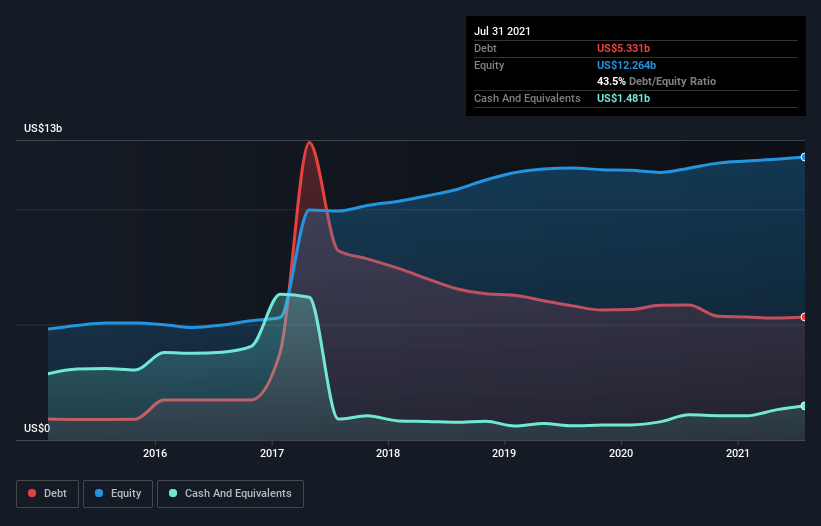

You can click the graphic below for the historical numbers, but it shows that Analog Devices had US$5.33b of debt in July 2021, down from US$5.85b, one year before. However, it also had US$1.48b in cash, and so its net debt is US$3.85b.

How Healthy Is Analog Devices’ Balance Sheet?

The latest balance sheet data shows that Analog Devices had liabilities of US$2.79b due within a year, and liabilities of US$6.58b falling due after that. Offsetting these obligations, it had cash of US$1.48b as well as receivables valued at US$823.2m due within 12 months. So its liabilities total US$7.07b more than the combination of its cash and short-term receivables.

Given Analog Devices has a humongous market capitalization of US$101.5b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Analog Devices has a low net debt to EBITDA ratio of only 1.3. And its EBIT easily covers its interest expense, being 12.0 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. In addition to that, we’re happy to report that Analog Devices has boosted its EBIT by 44%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Analog Devices’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Analog Devices actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

The good news is that Analog Devices’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Considering this range of factors, it seems to us that Analog Devices is quite prudent with its debt, and the risks seem well managed.