Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, American Water Works Company, Inc. (NYSE:AWK) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is American Water Works Company’s Debt?

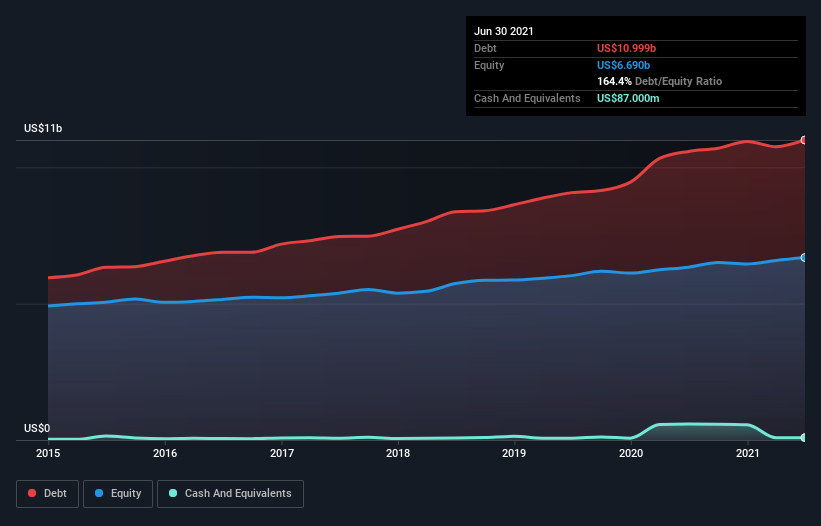

As you can see below, American Water Works Company had US$11.0b of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. And it doesn’t have much cash, so its net debt is about the same.

How Healthy Is American Water Works Company’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that American Water Works Company had liabilities of US$1.71b due within 12 months and liabilities of US$16.6b due beyond that. Offsetting these obligations, it had cash of US$87.0m as well as receivables valued at US$565.5m due within 12 months. So it has liabilities totalling US$17.6b more than its cash and near-term receivables, combined.https://b8605c50fa07feb9589ab7fe82daf47f.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

This deficit isn’t so bad because American Water Works Company is worth a massive US$31.6b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

American Water Works Company has a rather high debt to EBITDA ratio of 5.6 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 3.3 times, suggesting it can responsibly service its obligations. The good news is that American Water Works Company improved its EBIT by 4.8% over the last twelve months, thus gradually reducing its debt levels relative to its earnings. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine American Water Works Company’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, American Water Works Company burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both American Water Works Company’s net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. It’s also worth noting that American Water Works Company is in the Water Utilities industry, which is often considered to be quite defensive. Looking at the bigger picture, it seems clear to us that American Water Works Company’s use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses.