Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Air Products and Chemicals, Inc. (NYSE:APD) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Air Products and Chemicals Carry?

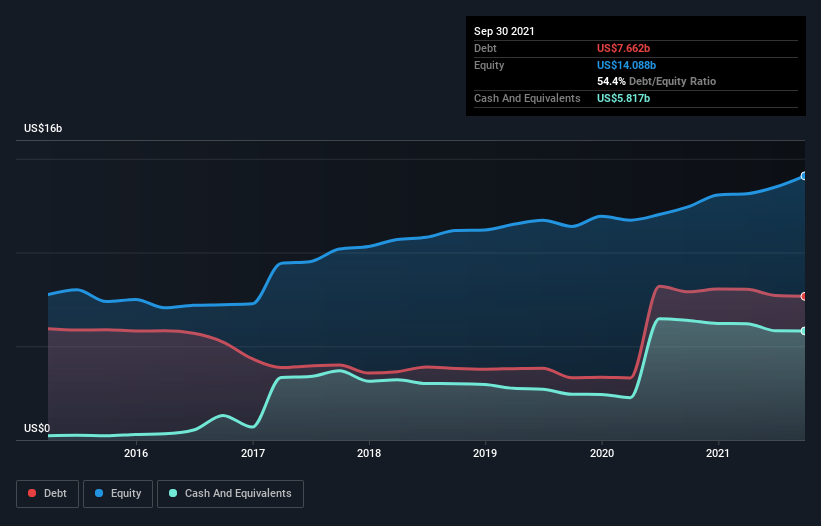

The chart below, which you can click on for greater detail, shows that Air Products and Chemicals had US$7.66b in debt in September 2021; about the same as the year before. However, it does have US$5.82b in cash offsetting this, leading to net debt of about US$1.85b.

How Strong Is Air Products and Chemicals’ Balance Sheet?

The latest balance sheet data shows that Air Products and Chemicals had liabilities of US$2.80b due within a year, and liabilities of US$9.97b falling due after that. Offsetting this, it had US$5.82b in cash and US$1.66b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$5.30b.

Given Air Products and Chemicals has a humongous market capitalization of US$65.9b, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Air Products and Chemicals has a low net debt to EBITDA ratio of only 0.50. And its EBIT easily covers its interest expense, being 16.6 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, Air Products and Chemicals grew its EBIT by 4.8% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Air Products and Chemicals’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Air Products and Chemicals’s free cash flow amounted to 39% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Air Products and Chemicals’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its net debt to EBITDA is also very heartening. Looking at all the aforementioned factors together, it strikes us that Air Products and Chemicals can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start.