Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Prestige Consumer Healthcare Inc. (NYSE:PBH) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

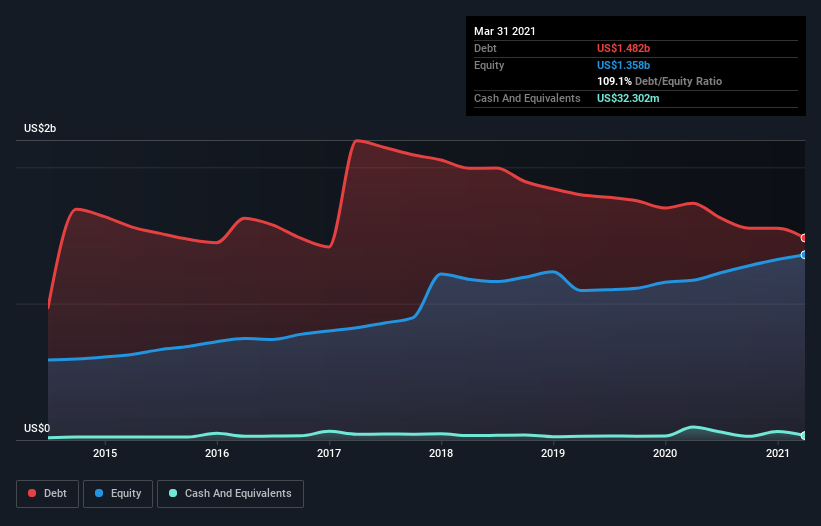

What Is Prestige Consumer Healthcare’s Net Debt?

As you can see below, Prestige Consumer Healthcare had US$1.48b of debt at March 2021, down from US$1.74b a year prior. On the flip side, it has US$32.3m in cash leading to net debt of about US$1.45b.

A Look At Prestige Consumer Healthcare’s Liabilities

According to the last reported balance sheet, Prestige Consumer Healthcare had liabilities of US$122.1m due within 12 months, and liabilities of US$1.95b due beyond 12 months. Offsetting these obligations, it had cash of US$32.3m as well as receivables valued at US$114.7m due within 12 months. So it has liabilities totalling US$1.92b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$2.50b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Prestige Consumer Healthcare’s debt is 4.4 times its EBITDA, and its EBIT cover its interest expense 3.6 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Fortunately, Prestige Consumer Healthcare grew its EBIT by 2.1% in the last year, slowly shrinking its debt relative to earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Prestige Consumer Healthcare’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Prestige Consumer Healthcare produced sturdy free cash flow equating to 67% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Neither Prestige Consumer Healthcare’s ability handle its debt, based on its EBITDA, nor its interest cover gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. Taking the abovementioned factors together we do think Prestige Consumer Healthcare’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. There’s no doubt that we learn most about debt from the balance sheet.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.